At its core, accounting is the process of recording, summarising, and reporting a company’s financial transactions. But that’s a textbook definition. In reality, it’s the language of your business, translating every sale, purchase, and payment into clear insights that shape your strategy. For any business in the UAE, getting this right isn’t just good practice—it’s absolutely essential for survival and growth.

Why Business Accounting Is Your Strategic Compass

Too many entrepreneurs see accounting as a chore, a box-ticking exercise to keep the authorities happy. This view completely misses the point and the power behind the numbers.

Think of your business as a ship navigating the competitive waters of the UAE market. Your accounting system is your entire navigation suite—your compass, your sonar, your GPS. It’s what gives you the critical data you need to chart a successful course.

It shows you exactly where you’ve been by organising historical financial data. It tells you where you are right now, offering a real-time snapshot of your company’s health. Most importantly, it helps you map out where you want to go, allowing you to set realistic goals for growth and profitability.

The Pillars of Strategic Accounting

For your accounting to be a reliable compass, it needs to stand on three interconnected pillars. Each one plays a distinct role in turning raw financial data into actionable intelligence. When they work together seamlessly, you get the clarity needed for sharp decision-making, attracting investors, and building a truly resilient business.

These core pillars are:

- Bookkeeping: This is the foundation. It’s the meticulous, day-to-day recording of every single transaction—every sale, every invoice paid, every expense incurred. Get this wrong, and everything else that follows will be built on shaky ground.

- Reporting: This is where the raw data gets turned into something useful. Reporting involves summarising all that bookkeeping information into financial statements, like the income statement and balance sheet. These reports are the maps that show your performance and financial position.

- Compliance: This pillar ensures all your financial activities are in line with UAE regulations, from VAT laws to the new Corporate Tax requirements. Proper compliance isn’t just about avoiding penalties; it’s about building trust with banks, investors, and government bodies.

Your financial records do more than just meet legal obligations; they tell the story of your business. A clear, accurate, and well-managed accounting system is often the first thing potential investors and lenders will examine.

From Compliance to Competitive Advantage

Ultimately, mastering your business’s finances is about gaining control. When you have a firm grip on your cash flow, profitability, and expenses, you stop making reactive guesses and start making proactive, informed decisions.

A solid understanding of the rules, like Mastering Revenue Recognition Principles, is fundamental to painting an accurate picture of your performance. These accurate records let you spot trends, pinpoint where money is being wasted, and jump on opportunities faster than your competitors. In the dynamic UAE market, that capability isn’t just an advantage; it’s a necessity for long-term success.

Mastering Financial Compliance in the UAE

Navigating the business world of the UAE is about more than just a great idea. It demands a rock-solid understanding of financial compliance. This isn’t some optional extra; it’s the very foundation that supports your entire operation, ensuring you operate legally and build a trustworthy reputation from day one.

Think of mastering compliance like knowing the rules of the road before you even turn the key. From tax obligations to record-keeping mandates, each regulation is a critical piece of your business puzzle. Ignoring them can lead to hefty penalties, operational headaches, and serious damage to your company’s standing with authorities, banks, and investors.

This is your roadmap to building and maintaining a bulletproof financial framework, making sure your business is not just profitable, but resilient for the long haul.

Understanding Value Added Tax (VAT)

Value Added Tax, or VAT, is a cornerstone of the UAE’s financial system. It was introduced back in 2018 and is essentially a tax on the consumption of most goods and services. For any business here, getting your head around VAT obligations is non-negotiable, and it all starts with knowing when to register.

Currently, it’s mandatory for a business to register for VAT if its taxable supplies and imports top AED 375,000 over a year. You can also choose to register voluntarily if your supplies or expenses exceed AED 187,500. This can be a smart strategic move, as it allows you to start reclaiming the VAT you pay on your own business expenses.

Once you’re registered, you have a few key responsibilities:

- Charging VAT: You’ll need to apply the standard 5% rate to your taxable goods or services.

- Issuing tax-compliant invoices: All your invoices must meet the specific requirements laid out by the Federal Tax Authority (FTA).

- Filing VAT returns: You’ll submit regular returns (usually every quarter) to the FTA, detailing the VAT you’ve collected versus the VAT you’ve paid.

Getting VAT management right is crucial. For a deeper dive into all your obligations, check out our complete guide on UAE tax services and compliance.

The Chart of Accounts and Record Retention

Beyond taxes, your internal accounting structure needs to be up to local standards. The Chart of Accounts (CoA) is the backbone of your entire financial recording system. It’s a complete list of every single account in your general ledger, neatly organised into categories like assets, liabilities, equity, revenue, and expenses. A well-structured CoA tailored for the UAE makes your financial reporting clear, consistent, and fully compliant.

Just as important is how long you hold onto your financial records. UAE law is clear: businesses must retain their records for a minimum of five years.

This five-year retention policy isn’t just about stashing old invoices in a filing cabinet. It’s about maintaining a complete, auditable history of your business’s financial journey, which is absolutely essential for audits, legal disputes, or any future due diligence.

This push towards structured compliance reflects a much bigger trend in the region. The Middle East and North Africa (MENA) region has seen a major drive to adopt global accounting standards. In fact, nearly all jurisdictions are now aligning with frameworks like International Financial Reporting Standards (IFRS), a move that boosts transparency and investor confidence across the board. You can discover more insights about this trend toward international standards adoption on ifac.org.

When Is an External Audit Required?

An external audit is an independent examination of your financial statements, carried out by a certified auditor. While not every single business in the UAE needs one every year, it becomes a necessity under certain conditions, especially for companies operating on the mainland or in certain free zones.

An audit might be mandatory if:

- Your company’s memorandum of association requires one.

- You are a publicly listed company or a regulated entity like a bank.

- Your free zone authority mandates an audit as part of your licence renewal.

Even when it’s not legally required, a voluntary audit can add tremendous credibility to your business. It provides assurance to shareholders, lenders, and potential investors that your financial statements are accurate and fairly presented. Think of it as a professional seal of approval on your financial health, one that can open doors to new financing and partnership opportunities. Staying ahead of these requirements helps you manage your obligations without any last-minute surprises.

Building Your Daily Bookkeeping System

Great accounting isn’t about memorising complex theories; it’s about the simple, consistent habits you practice every single day. Let’s move from the ‘what’ to the ‘how’ and outline a solid bookkeeping system you can start using immediately. Think of it as creating a rhythm for your finances, turning what feels like a chore into a powerful engine that feeds your business real, actionable data.

The first habit, and by far the most important, is to track every single dirham that moves. Every invoice you send, every payment you get, every expense you incur—it all needs to be recorded. This is more than just throwing receipts in a shoebox; it’s about building a live, accurate financial picture of your business at any given moment.

A non-negotiable rule here is the strict separation of your personal and business finances. Mixing them up is the fastest way to create a mess, leading to tax headaches and a complete loss of clarity on how your company is actually performing. For more on setting up the right accounts, check out our guide on opening a business bank account: https://alainbcenter.com/non-resident-bank-account-dubai/.

The Daily Workflow: From Document to Data

A smooth bookkeeping workflow is all about capturing financial information right at the source and turning it into something useful. This process boils down to a few logical, repeatable steps that, when done consistently, become the heartbeat of your financial operations.

The workflow always starts with the source documents:

- Capture Everything: The process kicks off the second a transaction happens. This means capturing every invoice, receipt, and bank statement. Modern apps are a game-changer here—you can just snap a photo of a receipt with your phone, instantly digitising it and saving it from getting lost.

- Record Accurately: Next, you need to categorise and record each transaction in your accounting software. Was that purchase for office supplies or marketing materials? Getting this right is crucial for pulling meaningful reports later.

- Reconcile Regularly: At least weekly, if not more often, you must reconcile your books. This means matching the transactions in your accounting software against your actual bank statements. It ensures every dirham is accounted for and that your records are 100% accurate.

Think of bank reconciliation as a quality control check for your money. It’s how you confirm that your records perfectly mirror the bank’s, catching any potential errors, odd transactions, or hidden bank fees before they snowball into bigger problems.

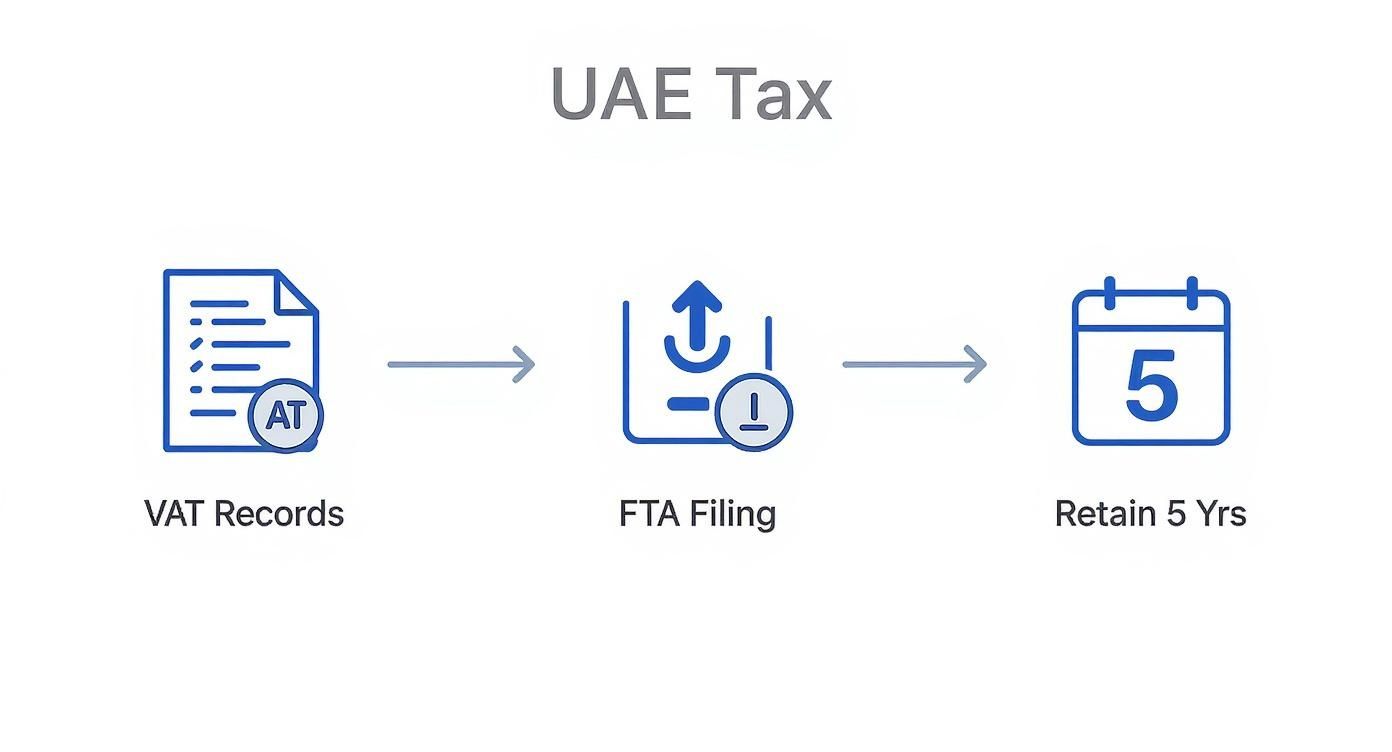

This disciplined process is exactly what keeps your VAT records clean and ready for filing with the FTA, a critical part of staying compliant in the UAE. The infographic below shows this simple but essential tax compliance cycle.

This image perfectly illustrates the non-negotiable journey from maintaining VAT-compliant records to filing on time with the FTA and sticking to the mandatory five-year retention period.

Using Technology to Work Smarter, Not Harder

Let’s be honest, doing all of this manually is a recipe for headaches and human error. Thankfully, modern technology can handle most of the heavy lifting, turning a tedious job into an efficient process that hums along in the background. Cloud accounting software is the heart of any modern system.

These platforms can automatically import bank transactions, learn how you categorise recurring expenses, and whip up professional invoices in seconds. A huge time-saver is automating invoice processing, which drastically cuts down on manual effort and boosts accuracy across the board.

This kind of automation frees you from the drudgery of data entry. Instead of spending hours logging receipts, you can spend minutes reviewing your profit and loss statement to make smarter, data-driven decisions that actually move your business forward. And that’s the whole point—your bookkeeping system should provide real-time intelligence, not just a history lesson.

How to Choose the Right Accounting Software

Picking the right technology is easily one of the most critical financial decisions you’ll make for your business. Good accounting software is so much more than a digital ledger; it’s the operational heart of your company. It automates mind-numbing tasks, gives you instant clarity on your financial health, and keeps you compliant with UAE regulations.

It’s the difference between reactive bookkeeping—a chore you dread—and proactive financial strategy that fuels your growth.

The market is full of excellent cloud-based platforms, but the best one for you comes down entirely to your specific business needs. It’s easy to get distracted by flashy feature lists, but the real focus should be on practical tools that solve the day-to-day challenges of running a business here in the UAE.

Core Features for UAE Businesses

Before you start comparing brand names, let’s establish the absolute non-negotiables. Any software you’re seriously considering must nail these three fundamentals.

- FTA Compliance: This is the big one. The platform absolutely must be compliant with the Federal Tax Authority (FTA). That means generating VAT-compliant invoices, creating flawless VAT return reports, and being able to produce an FTA audit file at a moment’s notice. This isn’t a nice-to-have; it’s your baseline requirement.

- Multi-Currency Support: Dubai is a global hub, so dealing with transactions in different currencies like USD, EUR, or GBP is just part of doing business. Your software needs to handle multiple currencies without breaking a sweat, applying real-time exchange rates and giving you an accurate picture of your finances.

- Local Integrations: The software has to play nicely with local UAE banks and the payment gateways you use. Smooth connections simplify bank reconciliation and speed up the process of getting paid, which directly improves your cash flow.

Your accounting software should act as a bridge, not an island. Its ability to integrate with the tools you already use—from your bank to your e-commerce platform—is what unlocks true efficiency and creates a single source of truth for your financial data.

Evaluating the Top Contenders

In the UAE, the conversation about cloud accounting software usually revolves around three major players: Zoho Books, Xero, and QuickBooks Online. While all three are powerful tools, they’re each built for slightly different types of businesses. Figuring out their unique strengths is the key to choosing one that will grow with you.

It’s also worth noting that these platforms are getting smarter by the day. The AI in accounting market in the Middle East and Africa is set for a massive surge, projected to grow from USD 303.3 million in 2024 to an incredible USD 9,645.0 million by 2033. This means the software you choose today will likely offer incredibly powerful automation and predictive insights down the line. You can explore the full research on AI’s impact on regional accounting on grandviewresearch.com.

Making the Final Choice

To help you decide, let’s break down how each platform stacks up against key business needs. The right software for a solo freelancer is very different from what a growing SME with ten employees needs.

I’ve put together a simple comparison to give you a bird’s-eye view of the landscape.

Comparing Top Accounting Software for UAE Businesses

This table outlines the key features and ideal use cases for the leading cloud accounting platforms available to businesses in the UAE.

| Feature | Zoho Books | Xero | QuickBooks Online |

|---|---|---|---|

| Best For | Start-ups and SMEs looking for an all-in-one ecosystem. | Businesses prioritising a vast app marketplace and scalability. | Service-based businesses and those familiar with the QuickBooks interface. |

| FTA Compliance | Excellent, with dedicated UAE version and features. | Strong, with comprehensive VAT reporting and audit file generation. | Good, with solid VAT tracking and filing capabilities. |

| Scalability | High, integrates deeply with other Zoho apps (CRM, Inventory). | Very high, supports unlimited users and extensive third-party apps. | Moderate, best suited for small to medium-sized operations. |

| Ease of Use | Clean interface, generally intuitive for new users. | Modern and user-friendly, praised for its design. | Can have a steeper learning curve but is powerful once mastered. |

| Cost | Highly competitive pricing, often the most affordable option. | Mid-range pricing, with costs increasing based on features. | Tends to be at the higher end of the price spectrum. |

Ultimately, the best accounting software is the one you and your team will actually use every day. Don’t skip the free trials! Get in there, test the interface, and see which workflow feels the most natural. That hands-on experience is the best way to choose a real partner for your business’s financial journey.

Deciding Between In-House and Outsourced Accounting

Sooner or later, every business owner faces a critical financial fork in the road. Do you build your own accounting team from the ground up, or do you bring in an external firm? There’s no single right answer here—it’s not a one-size-fits-all situation. The best path for you hinges entirely on your company’s size, complexity, budget, and where you see it going in the future.

Getting this decision wrong can be costly, leading to wasted money, compliance headaches, and even holding back your growth. But get it right, and you’ll have a rock-solid financial backbone that supports your business as it expands. Let’s walk through both options to see which makes the most sense for your UAE operation.

The Case for an In-House Accounting Team

Hiring an in-house accountant essentially means bringing all your financial management under your own roof. The biggest advantage? Direct control and deep integration. An in-house professional lives and breathes your business, learning its unique rhythms, challenges, and opportunities from the inside.

They become a true part of your company culture, available for a quick question down the hall or to sit in on strategic planning sessions. This kind of immersion means they can often spot issues or opportunities an outsider might miss.

Of course, that level of control comes with a hefty price tag that goes well beyond a monthly salary.

- Financial Commitment: You’re on the hook for salary, visa costs, medical insurance, end-of-service gratuity, and all the other allowances required by UAE labour law.

- Ongoing Training: The worlds of accounting and tax are always in flux. You’ll need to invest in continuous professional development to keep your team’s knowledge sharp.

- Resource Management: You also need to supply the tools for the job, like accounting software subscriptions, office space, and IT support.

For larger, more established companies with a high volume of complex daily transactions, building an in-house team is often the logical next step. Having a dedicated person on-site is simply essential for keeping operations running smoothly.

The Power of Outsourced Accounting Services

The alternative is to partner with a specialised firm that handles all your accounting needs remotely. This model has exploded in popularity, especially for start-ups and SMEs here in the UAE. The primary appeal is simple: you get access to a team of experts without the heavy financial weight of full-time employees.

When you outsource, you aren’t just getting one person—you’re tapping into a whole team of bookkeepers, senior accountants, and tax specialists. This collective know-how is priceless for navigating the fine print of UAE compliance, from VAT filings to the new Corporate Tax landscape.

Outsourcing transforms accounting from a fixed overhead cost into a scalable, operational expense. You pay only for the services you need, allowing you to ramp up or scale down your support as your business evolves.

This approach offers incredible flexibility and is extremely cost-effective. A good firm brings proven processes and top-tier software to the table, often delivering a higher level of efficiency than a small in-house team ever could. This is especially true in a region where solid financial systems are non-negotiable.

The wider economic picture in MENA shows just how important this is, with adult account ownership jumping from 43% in 2014 to 53% in 2024. This trend underscores the growing need for accurate, professional financial reporting. You can read more about these key financial inclusion findings from the World Bank.

The main thing to keep in mind with outsourcing is the potential for less direct oversight. That’s why it’s crucial to pick a reputable partner with fantastic communication, ensuring you always have a clear picture of your finances.

Comparing Your Options: A Financial Snapshot

To make this decision less abstract, let’s crunch some numbers. While the exact figures will vary based on experience and scope, this gives you a realistic idea of the financial commitment for each path.

| Cost Component | In-House Accountant (Annual Estimate) | Outsourced Firm (Annual Estimate) |

|---|---|---|

| Salary / Service Fee | AED 96,000+ | AED 24,000+ |

| Visa & Insurance | AED 8,000 | Included in Fee |

| Software & Tools | AED 3,000 | Included in Fee |

| Training & Development | AED 2,500 | Included in Fee |

| End-of-Service Provision | ~AED 8,000 | Not Applicable |

| Total Estimated Cost | AED 117,500+ | AED 24,000+ |

The table makes the cost difference crystal clear. For most start-ups and SMEs, outsourcing offers access to professional-grade accounting for a fraction of what it costs to hire a single person. This frees up vital capital that you can pump back into growing your business—think marketing, product development, and sales. Ultimately, the right choice is the one that best fits your budget today and your ambitions for tomorrow.

Streamlining Your Business with Integrated Services

Running a business in the UAE means you’re constantly juggling. You’ve got accounting to guide your big-picture strategy, bookkeeping to stay compliant, and a mountain of admin just to keep the lights on. Trying to manage each of these separately isn’t just inefficient; it pulls you away from what you should be doing—growing your business.

This is exactly where an integrated service partner changes the game.

Instead of seeing accounting as just another box to tick, this approach weaves it into the day-to-day operations of your company. This creates a seamless support structure for your business, cutting through the complexity so you can pour your energy back into innovation.

At Al Ain Business Centre, our accounting and bookkeeping packages are built to do more than just meet deadlines. We aim to deliver real, actionable financial intelligence that shapes your most critical decisions. Your financial data becomes a powerful tool for growth, not just a record of the past.

The Power of a Unified Approach

Think about it—real efficiency happens when your financial management and administrative tasks are perfectly in sync. Imagine your accounting team having instant access to the same experts who handle your visa renewals and regulatory approvals. No more communication breakdowns or chasing paperwork. Everything is aligned.

That’s the kind of synergy we create by combining professional accounting with expert PRO services. Our teams work hand-in-hand to lift the essential administrative burdens that can so easily trip up a growing business.

This integrated model delivers some pretty clear benefits:

- A Single Point of Contact: You get one dedicated partner managing multiple core functions, which means simpler communication and clearer accountability.

- Less Administrative Hassle: We take on the time-sucking paperwork, from financial reports to government liaison, freeing you and your team to focus on bigger things.

- Stronger Compliance: With a unified team, we ensure both your financial and administrative activities are completely in line with all UAE regulations.

- Holistic Business Insight: We see the full picture of your operations, which allows us to offer more strategic and genuinely useful advice.

An integrated service model turns your essential support functions from a scattered list of costs into a single, strategic investment. It builds an operational foundation that’s not just efficient today, but also ready to scale as you grow.

This unified approach gives you a smooth, uninterrupted operational structure. For instance, our team can expertly handle everything from your day-to-day bookkeeping to the often-complex world of document clearing and government approvals. When you trust these critical functions to a single, expert provider, you can get back to your main objective with confidence: driving your business forward.

Your Top UAE Business Accounting Questions Answered

Stepping into the world of business accounting in the UAE can feel like navigating a maze, especially if you’re a new entrepreneur. It’s completely normal to have a long list of questions. Getting clear, straightforward answers is the first step to feeling confident and starting off on the right foot.

Let’s clear up some of the most common queries we hear from business owners just like you.

What’s the Absolute Bare Minimum I Need to Do?

At the very least, every single business in the UAE has to keep accurate, up-to-date financial records. This isn’t just good practice; it’s the law. You must have a clear system for tracking all money coming in and going out, along with the supporting documents like invoices and receipts, all kept organised and ready to access.

Even if you’re a small startup not yet required to register for VAT, this basic record-keeping is non-negotiable. Think of it as building a solid foundation—it prepares you for future growth, makes any potential audits painless, and gives you the real numbers you need to make smart business decisions.

How Long Do I Have to Keep My Financial Records?

According to UAE federal law, you must hang on to all your financial records for at least five years after the end of the financial period they relate to. This covers everything from your general ledger and invoices to contracts and bank statements.

This five-year rule is a big deal for financial compliance here. It ensures everything is transparent and gives the authorities the ability to conduct a proper audit if they ever need to. Not following this can lead to some hefty penalties.

Do I Really Need to Bother with Accounting Software?

Technically, you could try to run your books on a spreadsheet, but we strongly advise against it. Modern, cloud-based accounting software isn’t a luxury; it’s an essential tool for any serious business today. It puts transaction recording on autopilot, makes bank reconciliation a breeze, and generates professional financial reports in just a few clicks.

Even more importantly, using FTA-approved software guarantees that your invoicing and VAT reporting are fully compliant. This saves you from making expensive mistakes and dealing with massive administrative headaches later on. An investment in the right software is really an investment in your company’s efficiency and accuracy.

Ready to build a solid financial foundation for your UAE business without getting tangled in the complexity? The experts at Al Ain Business Center offer complete accounting, bookkeeping, and PRO services to ensure you stay compliant and can focus on what you do best—growing your business. Learn how we can support your business today.